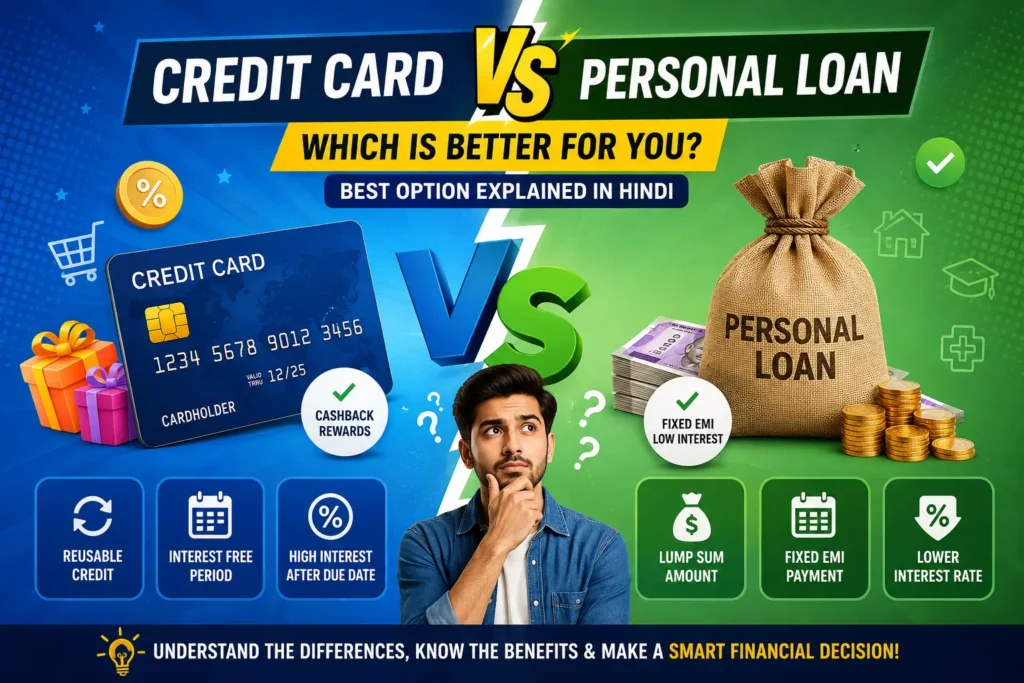

Confused between a Credit Card and a Personal Loan during a financial emergency? Don’t worry — this guide will help you understand the differences, advantages, disadvantages, and when to choose the right option for your needs.

🤔 Credit Card or Personal Loan: Which One Should You Choose?

Whenever there is an urgent need for money, the first two financial options that usually come to mind are Credit Cards and Personal Loans.

Both provide quick access to funds, and both are considered unsecured loans, meaning you do not need to provide collateral or security.

But here’s the big question:

Are Credit Cards and Personal Loans the Same?

Absolutely not!

Although both help during financial emergencies, they work very differently. Understanding these differences can help you avoid unnecessary debt and make smarter financial decisions.

In this blog, we’ll explain:

✔ What is a Credit Card?

✔ What is a Personal Loan?

✔ Their Advantages & Disadvantages

✔ Key Differences Between Both

✔ Which Option is Better for You?

💳 What is a Credit Card?

A Credit Card is basically a revolving credit system.

The bank gives you a spending limit — for example, ₹2 lakhs — and you can spend money according to your needs.

The best part?

🔄 Revolving Credit Facility

As soon as you repay the amount you spent, your credit limit becomes available again.

This means:

✅ No need to apply for a new loan repeatedly

✅ Quick access to money anytime

✅ Flexible spending

✨ Biggest Advantage of a Credit Card

🕒 Interest-Free Grace Period

Most credit cards offer a 45–50 day grace period.

If you repay the full amount within this period, you pay:

₹0 Interest

That means:

You borrowed money and returned it without paying interest — smart financial management!

🎁 Rewards, Cashback & Discounts

Another exciting benefit of credit cards is:

Cashback + Rewards + Discounts

Whenever you:

- Shop online or offline

- Pay bills

- Book travel tickets

- Make purchases

You can earn rewards and cashback.

Example:

Suppose you spent ₹20,000, and there is a 5% cashback offer.

You receive: ₹1,000 Cashback 💰

That’s money coming back into your pocket.

⚠️ Disadvantages of a Credit Card

While credit cards are convenient, they can become expensive if not used responsibly.

High Interest Rates After Grace Period

If you fail to pay the bill on time, the interest rate can go up to:

30%–36% annually. That’s extremely high.

If you are not financially disciplined, credit card debt can become costly.

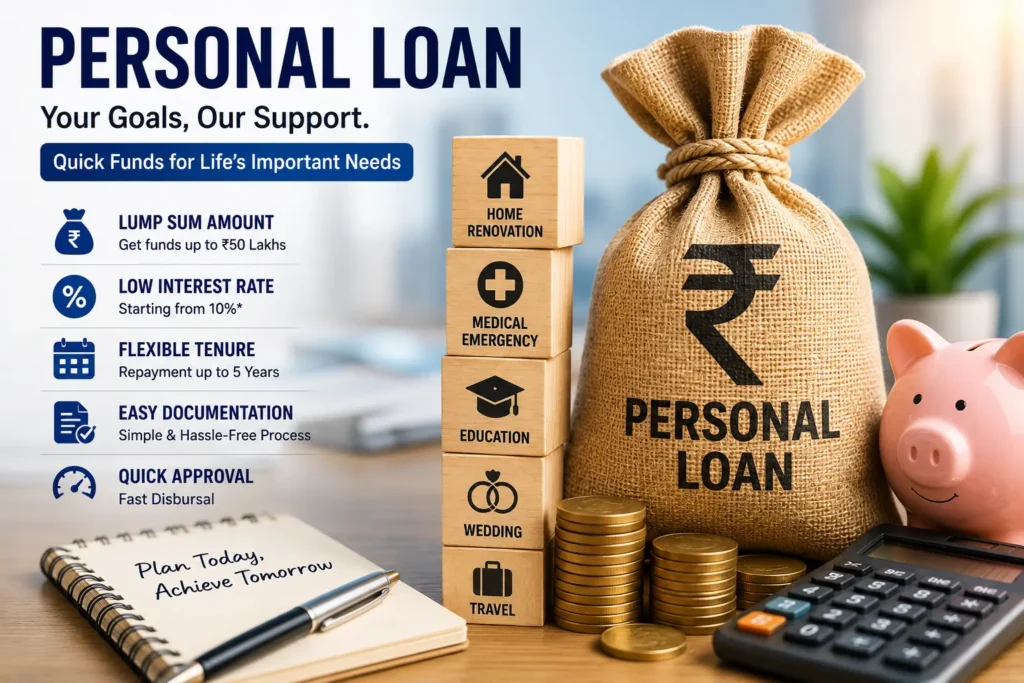

💸 What is a Personal Loan?

Unlike a credit card, a Personal Loan provides a lump sum amount in one go.

For example:

You may need money for:

- Home renovation 🏠

- Medical emergencies 🏥

- Wedding expenses 💍

- Education or urgent expenses

In such situations, a personal loan may be a better choice.

Example:

Suppose you need: ₹5 Lakhs

The bank provides the amount directly, and you repay it through monthly EMIs.

📄 Eligibility & Documentation for Personal Loan

Unlike credit cards, personal loans require documentation.

Banks generally ask for:

- Salary proof

- Bank statements

- PAN Card

- Aadhaar Card

- Employment proof

This means: More paperwork is involved.

📅 Repayment Tenure of Personal Loan

One major advantage of a personal loan is:

Long-Term Repayment

You can repay the amount through fixed monthly EMIs over a longer duration.

Usually: 1 Year to 5 Years

This makes repayment easier and more manageable.

📉 Interest Rate on Personal Loan

Compared to credit cards, personal loans generally have:

Lower Interest Rates

Typically: 10%–18% annually

This is much lower than the 30%–36% interest rate on credit cards.

✅ Biggest Advantage of Personal Loan

Fixed EMI = No Surprises

Every month, you pay a fixed EMI.

Benefits include:

✔ Predictable repayment

✔ Better financial planning

✔ No unexpected payment shock

Your loan gets cleared smoothly if managed properly.

⚠️ Drawback of Personal Loan

There is one downside.

Once you take a loan, you cannot reuse it instantly.

Unlike a credit card, there is:

❌ No revolving facility

If you need money again, you may need to:

- Reapply

- Submit documents again

- Complete paperwork

📊 Credit Card vs Personal Loan: Quick Comparison

| Feature | Credit Card | Personal Loan |

|---|---|---|

| Documentation | Minimal | Required |

| Loan Type | Revolving Credit | Lump Sum Amount |

| Interest Rate | 30%–36% | 10%–18% |

| Repayment | Flexible | Fixed EMI |

| Rewards & Cashback | Yes | No |

| Repeat Usage | Instant Reuse | New Application Required |

| Pre-Closure | Anytime | Charges May Apply |

🛒 When Should You Use a Credit Card?

A credit card is best when:

✅ You need a small amount of money

✅ You can repay within the grace period

✅ You want cashback and rewards

Example:

Suppose you buy gadgets worth ₹5,000, and your salary is coming next month.

In this case, A Credit Card is a Smart Option ✔

🏦 When Should You Take a Personal Loan?

A personal loan works better when:

✅ You need a large amount of money (₹3–5 lakhs or more)

✅ You want a comfortable EMI repayment

✅ You need long-term financial planning

✅ High credit card interest worries you

Example:

For:

- Medical emergencies

- Wedding expenses

- Major household expenses

Personal Loan is a Better Choice ✔

⚖️ Credit Card vs Personal Loan – Which is Better?

The answer depends on your financial needs.

Choose a Credit Card if:

✔ You are financially disciplined

✔ You can repay on time

✔ You need short-term funds

✔ You want cashback and rewards

Choose a Personal Loan if:

✔ You need a large amount of money

✔ You want lower interest rates

✔ You prefer fixed monthly EMIs

✔ You need long-term repayment comfort

💡 Final Thoughts

Both Credit Cards and Personal Loans have their own advantages and disadvantages.

If you are disciplined and make timely payments, a Credit Card can be a smart financial tool.

But if you need a large amount with comfortable repayment, a Personal Loan can be a better option.

Remember:

The right financial decision helps:

✅ Protect your credit score

✅ Reduce financial stress

✅ Improve financial planning

💬 Tell Us in the Comments!

In an emergency:

What would you choose?

Credit Card 💳 or Personal Loan 💸?

Let us know your thoughts!