Starting and growing a business is a dream for every entrepreneur. Whether you are a retailer, manufacturer, trader, or self-employed professional, expanding your business often requires additional funds. This is where a business loan becomes important.

However, many business owners face loan rejection due to a lack of understanding about bank eligibility criteria. Repeated loan rejections can even affect your credit score and reduce your chances of getting approved in the future.

In this detailed guide, we will explain everything you need to know about business loan eligibility criteria, common reasons for rejection, credit score requirements, and how you can improve your chances of approval.

Why Do Business Loans Get Rejected?

Many people believe that if one bank rejects their loan application, every bank will do the same. But that is not true.

Every bank and NBFC has different eligibility criteria. A loan rejected by one lender may still get approved by another.

The most common reasons for business loan rejection are:

- Poor credit score

- Low business vintage

- Weak financial records

- Declining turnover

- Incomplete documents

- Negative CIBIL history

- Poor banking transactions

Understanding these factors beforehand can save you from rejection and help you apply more effectively.

Who Can Apply for a Business Loan?

Business loans are available for various types of businesses and professionals.

Eligible Applicants Include:

- Retailers

- Manufacturers

- Traders

- MSMEs

- Small and large enterprises

- Partnership firms

- LLPs

- Private limited companies

- Self-employed professionals like doctors, consultants, and architects

Both new and existing businesses can apply for business loans. However, loans for new businesses are usually available under government schemes, while existing businesses can easily get loans from banks and NBFCs.

Types of Business Loans

Business loans are mainly divided into two categories:

1. Unsecured Business Loan

In this type of loan, no collateral or property is required.

Features:

- No security required

- Faster approval

- Popular among small business owners

- Higher interest rates compared to secured loans

2. Secured Business Loan

In a secured loan, you must provide security such as property, shop, factory, or land.

Features:

- Lower interest rates

- Higher loan amounts

- Longer repayment tenure

- Easier approval process

Eligibility Criteria for Unsecured Business Loans

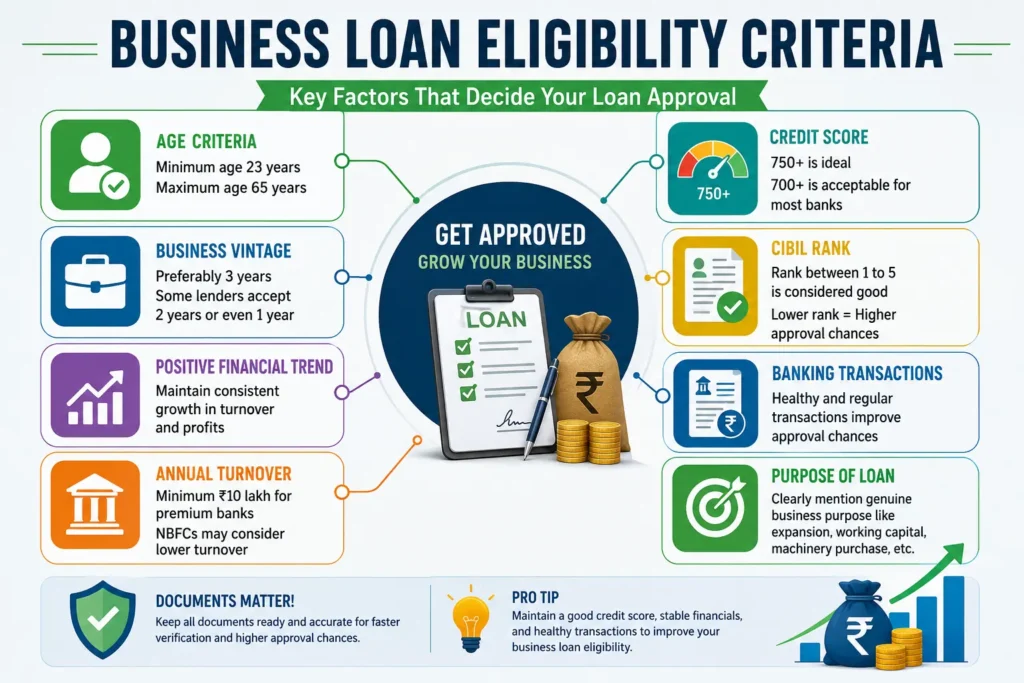

1. Age Requirement

Most banks require:

- Minimum age: 23 years

- Maximum age: 65 years

Some NBFCs may offer loans starting from 21 years of age.

2. Indian Nationality

The applicant must be an Indian citizen.

3. Business Vintage

Premium banks usually prefer businesses operating for at least 3 years.

However:

- Some NBFCs accept 2-year-old businesses

- P2P lending platforms may offer loans even after 1 year of business operations

4. Business Ownership Proof

Having assets in your name increases your chances of approval.

Examples include:

- House

- Shop

- Factory

- Godown

5. Positive Financial Trend

Banks prefer businesses showing steady growth.

For example:

- If your turnover was ₹2 crore last year and drops significantly this year, banks may consider your business unstable.

- Businesses with increasing turnover and profits are more likely to get approved.

Important Tip:

Some business owners reduce profits in ITRs to save taxes. While this may reduce tax liability, it can also reduce your loan eligibility.

6. Minimum Annual Turnover

Different lenders have different turnover requirements.

Generally:

- Premium banks may require ₹10 lakh or more annual turnover

- Some NBFCs offer loans even with ₹40–50 lakh turnover

- Certain lenders focus mainly on banking transactions instead of turnover

If your bank statements show healthy business activity, approval chances increase significantly.

Importance of Banking Transactions

Your bank statement plays a major role in loan approval.

Banks usually check:

- Regular business transactions

- Monthly cash flow

- Consistency in deposits

- Business income pattern

Premium banks often expect around 80% of your declared turnover to reflect in your bank account.

Credit Score: The Biggest Factor in Loan Approval

Your credit score is one of the most important factors for business loan approval.

Ideal Credit Score for Business Loans

- 750+ score = Excellent approval chances

- 700+ score = Good chances with most banks

- Below 700 = Difficult but possible through NBFCs or P2P lenders

Negative Statuses That Can Cause Rejection:

- Settlement

- Written-off accounts

- Loan defaults

- Late EMI payments

These negative remarks can make loan approval very difficult.

What is CIBIL Rank in Business Loans?

Just like individuals have a credit score, businesses have a CIBIL rank.

CIBIL Rank Range:

- 1 to 10

Best Rank:

- Rank between 1 to 5 is considered good

- Higher ranks reduce approval chances

Sometimes CIBIL reports contain errors due to:

- Data mismatch

- Wrong loan updates

- Delayed reporting by banks

If your report contains mistakes, you should rectify it before applying for a business loan

How to Improve Your Loan Approval Chances

Follow these important tips before applying:

Maintain a Good Credit Score

Always pay EMIs and credit card bills on time.

Show Consistent Turnover

Maintain stable or growing business income.

Keep Proper Banking Transactions

Avoid unnecessary cash transactions and maintain healthy bank activity.

File Accurate ITRs

Do not show extremely low profits just to save taxes.

Correct CIBIL Errors

Check your credit report regularly and fix any errors immediately.

Purpose of the Business Loan Matters

Banks often ask why you need the loan.

Good Loan Purposes Include:

- Business expansion

- Machinery purchase

- Working capital

- Inventory purchase

- Operational expenses

Avoid mentioning speculative or risky investments because banks may reject such applications.

Eligibility Criteria for Secured Business Loans

Secured business loans are easier to obtain because lenders have collateral security.

Basic Eligibility:

- Minimum age: 23 years

- Maximum age: 70 years

- Indian citizenship required

- Business vintage preferred: 2–3 years

Benefits of Secured Business Loans

Lower Interest Rates

Since property is pledged, lenders offer lower rates.

Higher Loan Amounts

You can get larger funding compared to unsecured loans.

Longer Repayment Tenure

This reduces EMI burden.

Flexible Approval

Even applicants with moderate credit scores may qualify.

Some NBFCs even approve secured loans for applicants with:

- 650+ credit score

- Moderate banking transactions

Property Requirements for Secured Loans

For secured business loans, the mortgaged property should:

- Be in the applicant’s name

- Have valid ownership documents

- Be legally clear

- Meet lender verification standards

Without proper legal documents, the loan may be rejected.

Documents Required for Business Loans

Whether secured or unsecured, you usually need:

- Aadhaar Card

- PAN Card

- Business registration proof

- Bank statements

- ITR documents

- GST returns

- Property documents (for secured loans)

Complete and accurate documentation improves approval speed.

Final Thoughts

Business loans are one of the best ways to expand and grow your business. However, understanding eligibility criteria before applying is extremely important.

A good credit score, stable business growth, healthy banking transactions, and proper documentation can significantly improve your chances of approval.

If your loan has been rejected before, do not lose hope. Work on improving your financial profile, correct your credit report if needed, and apply with the right lender.

With proper planning and preparation, getting a business loan becomes much easier.